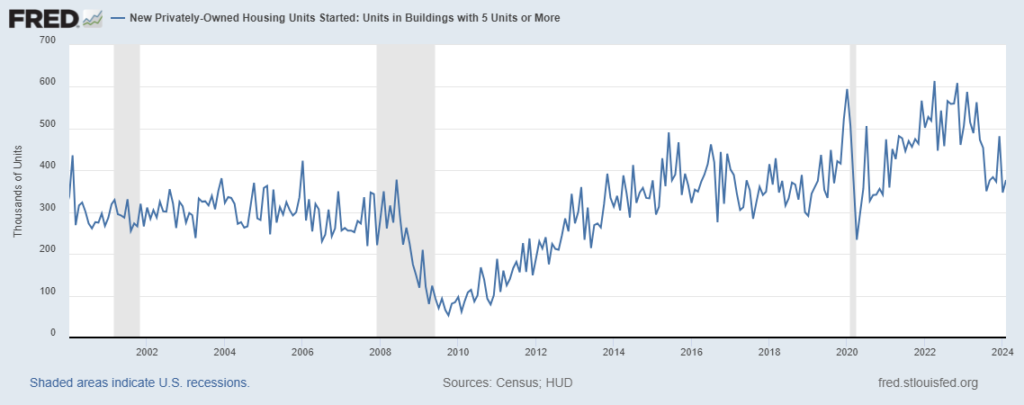

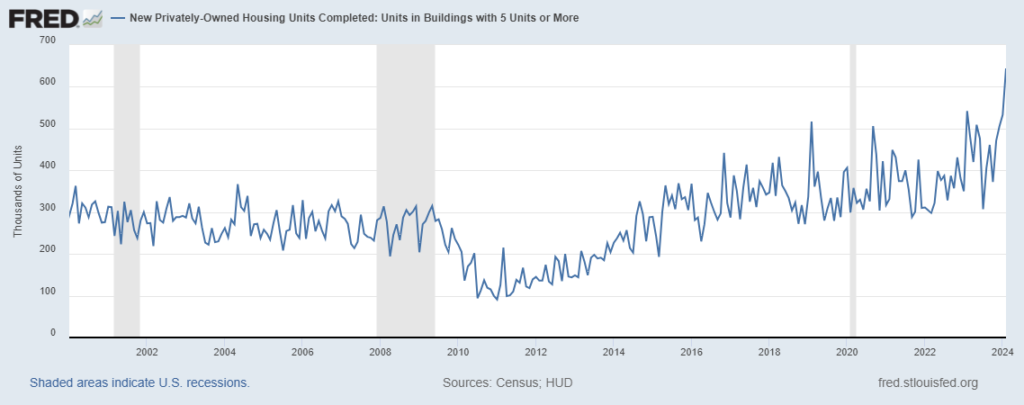

In these graphs you can see the spike in MF construction starts just after the post-pandemic ZIRP and QE, followed by the increase in completions ~24-36 months later. Eyeballing it, it looks like the higher level of starts lasted for about 18 months. So if the spike in completions began in Dec 2023, we should see increased supply of new MF come to market for the next year or so. As the Fed raised rates and bond yields increased, the number of starts fell dramatically. One cause for this is probably that projects that were previously viable at borrowing costs of 4-6% are not longer attractive at financing costs of 8-10%.